Macroeconomic Policy Bureau Weekly Economic Report as of December 17, 2021

Macroeconomic Policy Bureau Weekly Economic Report as of December 17, 2021

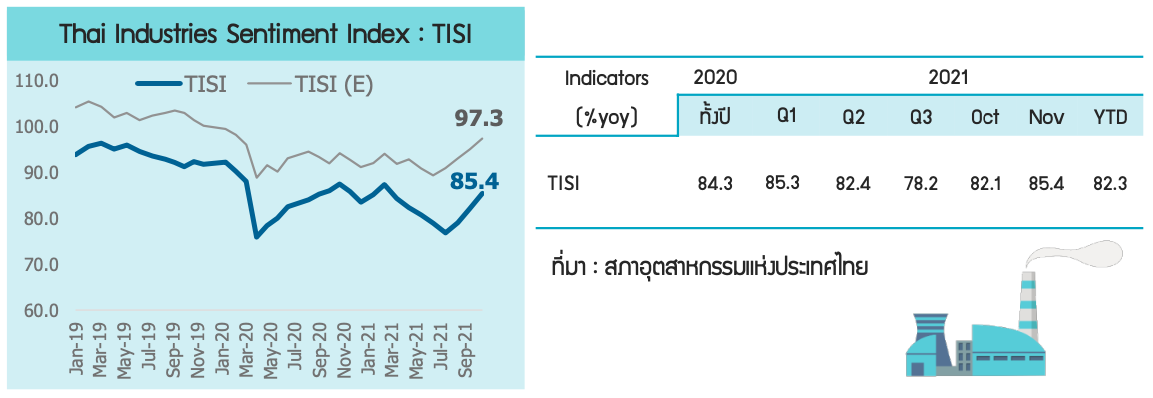

1. The Industrial Confidence Index (TISI) for November 2021 increased for the third consecutive month, reaching its highest level in eight months at 85.4, up from 82.1 in the previous month.

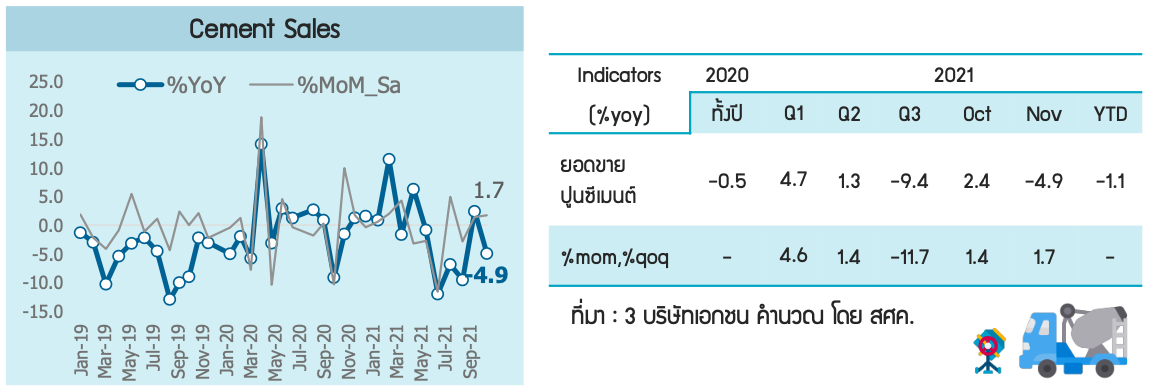

2. Domestic cement sales in November 2021 contracted by -4.9% compared to the same period last year.

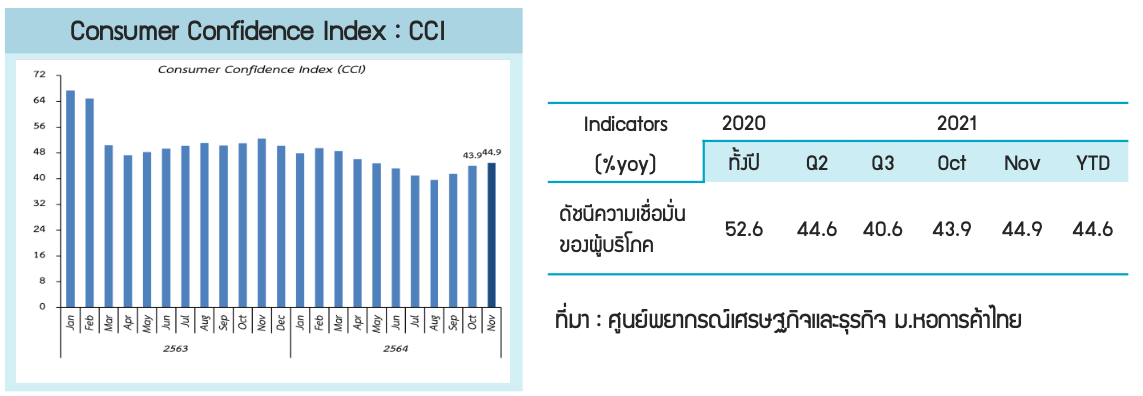

3. The Consumer Confidence Index in November 2021 rose to 44.9 from 43.9 in the previous month.

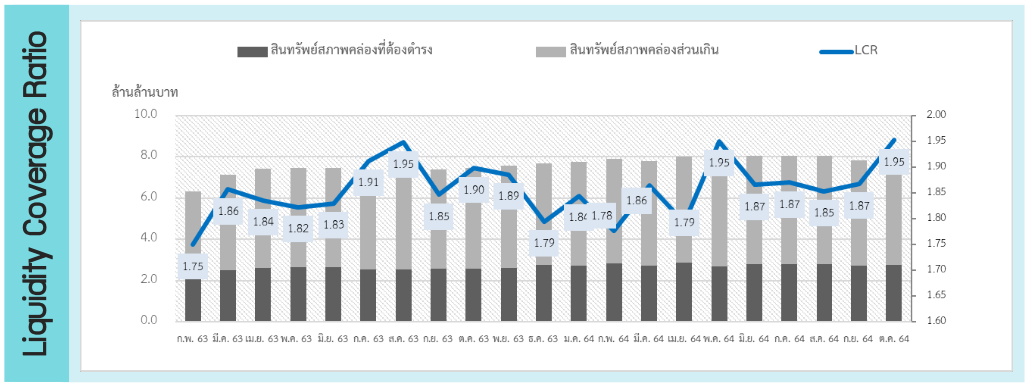

4. The liquidity asset level of commercial banks in October 2021 was 1.95 times the legally required liquidity assets.

Thai Economic Indicators

The Industrial Confidence Index (TISI) for November 2021 increased for the third consecutive month, reaching its highest level in eight months at 85.4, up from 82.1 in the previous month.

The index for November 2021 increased across all sizes of industries and regions compared to the previous month. Most components of the index improved, including overall orders, total sales, production volume, and performance, except for operational costs. This improvement was supported by the easing COVID-19 situation in the country, leading to a continuous recovery in economic activities, along with strong demand from abroad due to the recovery of key trading partners' economies, such as the U.S., China, ASEAN, and India. However, high raw material and energy costs continue to impact production and transportation costs, and the resurgence of COVID-19 in several countries may affect the export and manufacturing sectors.

Domestic cement sales in November 2021 contracted by -4.9% compared to the same period last year. However, when adjusted for seasonal effects, it showed a growth of 1.7% compared to the previous month.

In November 2021, cement sales contracted year-on-year due to production issues in some private companies, resulting in a slowdown in production and sales. Nevertheless, when considering month-on-month figures after seasonal adjustments, cement sales have increased for two consecutive months due to a resurgence in construction activities following the easing of the COVID-19 situation and flooding in several provinces. Looking ahead, there are still risks from the new COVID-19 variant that may impact economic activities, including construction.

The Consumer Confidence Index in November 2021 rose to 44.9 from 43.9 in the previous month, marking the third consecutive improvement and the highest level in seven months since May 2021.

This improvement is attributed to the easing of pandemic control measures by the CCSA to facilitate the reopening of the country starting November 1, 2021, allowing foreign tourists (from low-risk countries) to enter Thailand without quarantine. The CCSA also reduced the number of maximum and strict control areas (dark red), maximum control areas (red), controlled areas (orange), and high surveillance areas (yellow), while lifting the curfew to allow businesses and citizens to operate closer to normal levels, reducing economic and social impacts. This will be a key factor in gradually reviving economic activities.

Financial Sector Indicators

The liquidity asset level of commercial banks in October 2021 was 1.95 times the required liquidity assets.

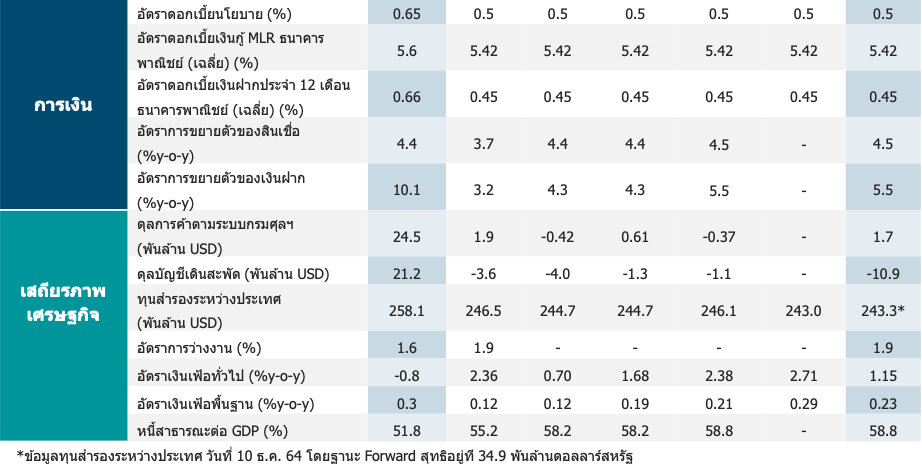

The total outstanding liquidity assets of commercial banks in October 2021 stood at 5.4 trillion baht, an increase from the previous month. The Bank of Thailand has adjusted the liquidity asset maintenance criteria for commercial banks from the previous requirement of maintaining liquidity assets at no less than 6% of deposits to no less than 100% (or 1.0 times) of the estimated net cash outflow in a crisis (Liquidity Coverage Ratio: LCR) since January 2016.

Source: Bank of Thailand

Thai Economic Indicators

United States

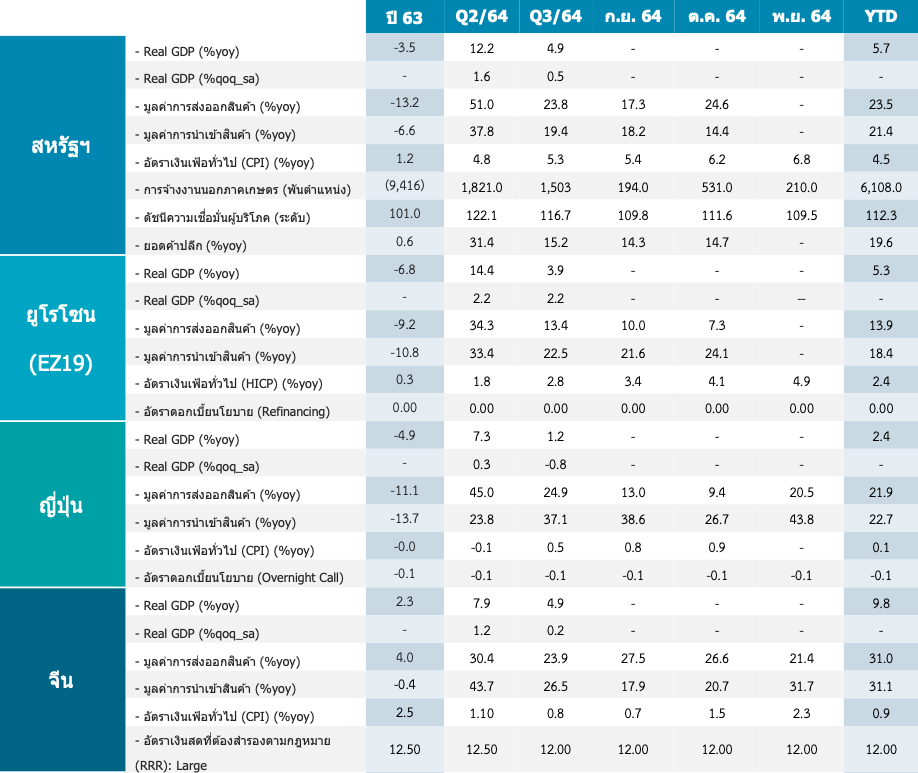

- Retail sales in November 2021 grew by 18.2% compared to the same period last year, accelerating from 16.3% growth in the previous month, marking the highest level in five months due to the onset of the year-end holiday season.

- Industrial production in November 2021 remained stable at 5.3% growth compared to the same period last year amid supply chain issues.

- New housing starts in November 2021 grew by 11.8% compared to the previous month (seasonally adjusted), reversing the -3.1% contraction from the previous month (seasonally adjusted), driven by strong growth across all types of new housing.

- New housing permits in November 2021 grew by 3.6% compared to the previous month (seasonally adjusted), slowing from 4.2% growth in the previous month (seasonally adjusted), due to a decline in townhome permits and a slowdown in single-family and condominium permits.

- The U.S. Federal Open Market Committee (FOMC) unanimously decided to maintain the policy interest rate at 0.00-0.25%, but will accelerate tapering by reducing government bond purchases by $20 billion per month and mortgage-backed securities purchases by $10 billion per month.

- The number of initial jobless claims for the week of December 5-11, 2021, was 206,000, an increase from 188,000 the previous week, but still below the pre-pandemic average of 220,000.

China

- Industrial production in November 2021 grew by 3.8% compared to the same period last year.

- This was an increase from 3.5% growth in the previous month, supported by a recovery in energy production and a decline in raw material prices.

- Retail sales in November 2021 grew by 3.9% compared to the same period last year, slowing from 4.9% growth in the previous month, due to reduced consumption amid the COVID-19 pandemic, particularly in jewelry, home appliances, telecommunications, and oil products.

- The unemployment rate in November 2021 was 5.0% of the total labor force, up from 4.9% in the previous month.

Eurozone

- The preliminary PMI for the manufacturing sector in December 2021 was at 58.0, down from 58.4 in the previous month, but still higher than the market expectation of 57.8.

- The preliminary PMI for the services sector in December 2021 was at 53.3, down from 55.9 in the previous month, due to the resurgence of COVID-19 in the European region.

- The European Central Bank decided to keep the policy interest rate at 0.0% per annum during its December 2021 meeting. Additionally, the ECB announced a reduction in the bond purchase program under the Pandemic Emergency Purchase Programme (PEPP) and will end this program in March 2022, stating that the recent increase in inflation is only temporary.

Hong Kong

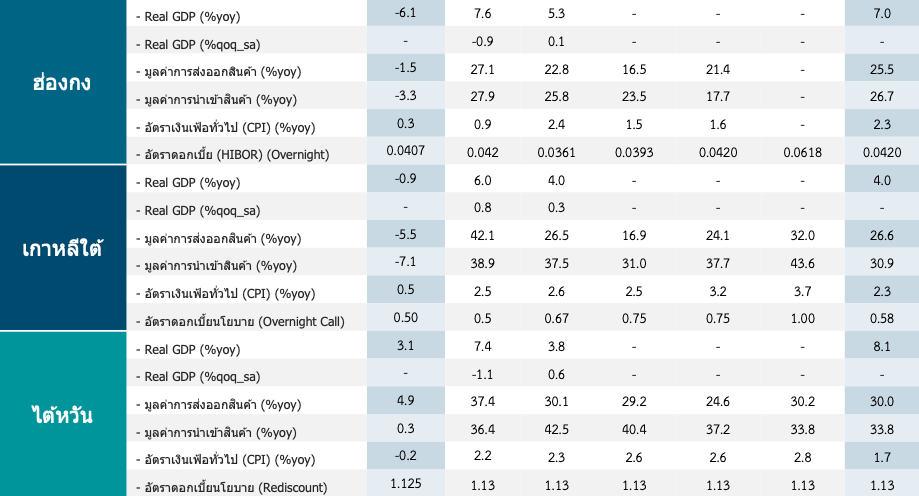

- Industrial production in Q3 2021 grew by 7.8% compared to the same period last year, accelerating from 5.6% growth in the previous quarter, marking the highest growth since Q4 2018, driven by increases in food, beverage, tobacco, and miscellaneous goods production.

- The unemployment rate in November 2021 was 4.1% of the total labor force, down from 4.3% in the previous month.

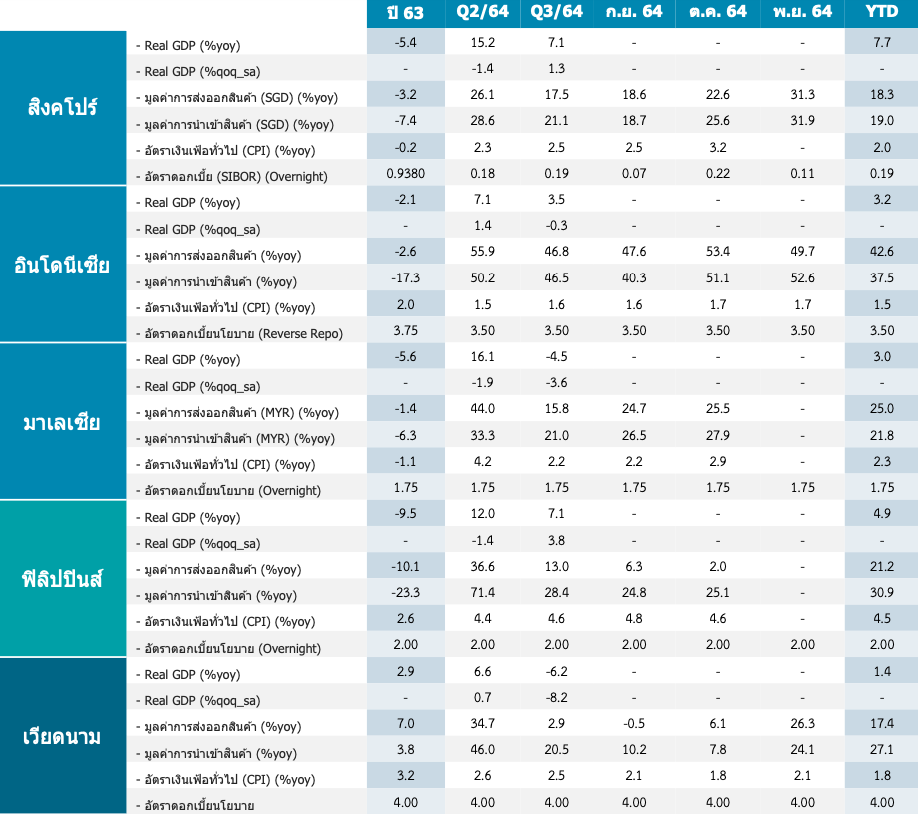

Singapore

- Export value in November 2021 grew by 31.3% compared to the same period last year, up from 22.6% growth in the previous month.

- Import value in November 2021 grew by 31.9% compared to the same period last year, up from 25.6% growth in the previous month.

- The trade balance in November 2021 recorded a surplus of SGD 6.24 billion, up from a surplus of SGD 5.9 billion in the previous month.

- The unemployment rate in Q3 2021 was 2.6% of the total labor force, down from 2.7% in the previous quarter.

Malaysia

- Export value in November 2021 grew by 49.7% compared to the same period last year, down from 53.4% growth in the previous month.

- Import value in November 2021 grew by 52.6% compared to the same period last year, up from 51.1% growth in the previous month.

- The trade balance in November 2021 recorded a surplus of USD 3.5 billion, down from a surplus of USD 5.7 billion in the previous month. The Bank of Indonesia announced to maintain the policy interest rate at 3.5% per annum to support economic recovery.

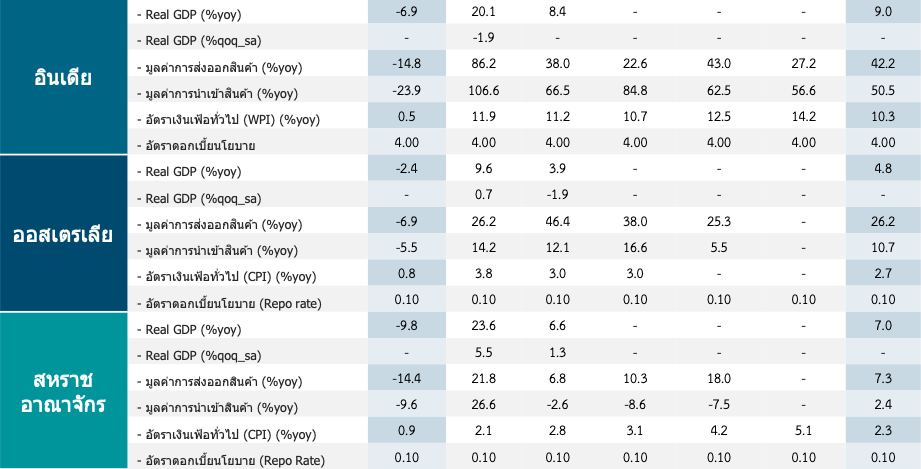

Australia

- The preliminary PMI for the manufacturing sector in December 2021 was at 57.4, down from 59.2 in November 2021, but still above the 50 mark, indicating continued expansion in the manufacturing sector.

- The preliminary PMI for the services sector in December 2021 was at 55.1, down from 55.7 in November 2021, marking the third consecutive month above the 50 mark, reflecting ongoing expansion in the services sector.

- The unemployment rate in November 2021 was 4.6% of the total labor force, down from 5.2% in October 2021, due to increased easing of COVID-19 control measures by the government.

Philippines

- The Bangko Sentral ng Pilipinas announced to maintain the policy interest rate at 2.0% per annum.

South Korea

- The unemployment rate in November 2021 was 3.1% of the total labor force, down from 3.2% in the previous month, supported by the easing of COVID-19 control measures and increased vaccination rates.

Taiwan

- The Central Bank of Taiwan announced to maintain the policy interest rate at 1.125% per annum.

United Kingdom

- The unemployment rate in October 2021 was 4.2% of the total labor force, down from 4.3% in September 2021, continuing a downward trend since December 2020.

- The inflation rate in November 2021 grew by 5.1% compared to the same period last year, up from 4.2% growth in October 2021, marking the highest growth since September 2011.

- The Bank of England decided to raise the policy interest rate to 0.25% per annum from 0.1% per annum during its December 2021 meeting to alleviate pressure from rising inflation. The preliminary PMI for the manufacturing sector in December 2021 was at 57.6, down from 58.1 in November 2021, aligning with market expectations of 57.6. The preliminary PMI for the services sector in December 2021 was at 53.2, down from 58.5 in November 2021, due to the impact of the Omicron variant of COVID-19 on economic activities in the services sector.

Money Market and Exchange Rate Indicators

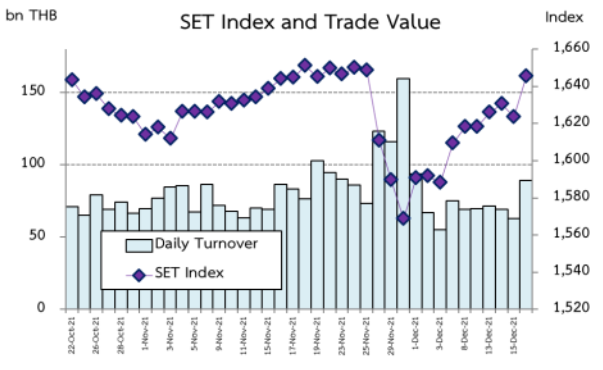

The SET index increased from the previous week, contrary to other regional stock markets that declined. On December 16, 2021, the index closed at 1,645.32 points with an average trading value between December 13-16, 2021, of 73.202 billion baht per day. Foreign investors and securities company accounts were net buyers, while domestic retail investors and domestic institutional investors were net sellers. During December 13-16, 2021, foreigners net purchased securities worth 8.531 billion baht.

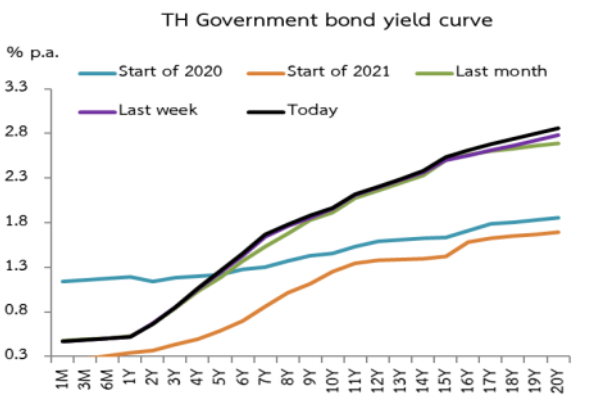

The overall yield on government bonds increased by 0 to 8 bps. This week, investors participated in the auction of 22-year government bonds, which attracted 1.79 times the auction amount. During December 13-16, 2021, net foreign capital inflow in the bond market was 6.064 billion baht, and since the beginning of the year until December 16, 2021, net foreign capital inflow in the bond market was 142.464 billion baht.

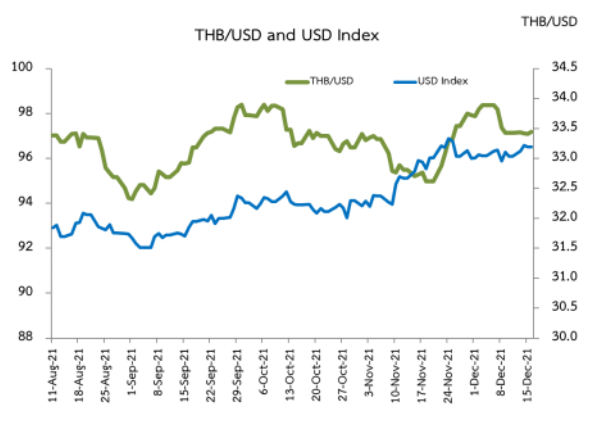

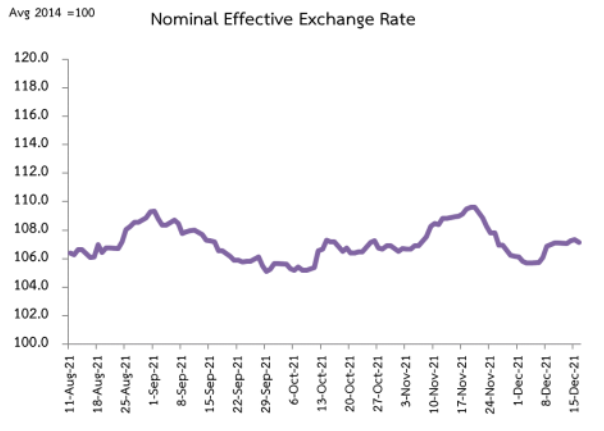

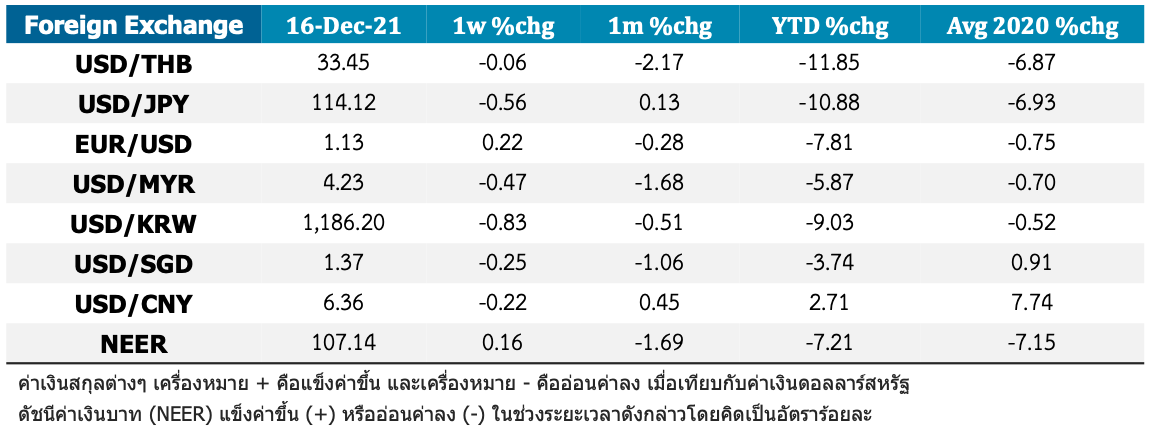

The Thai baht weakened against the previous week, closing at 33.45 baht per US dollar on December 16, 2021, a decrease of -0.06% from the previous week, aligning with the depreciation of the yen, ringgit, won, Singapore dollar, and yuan against the US dollar. Meanwhile, the euro appreciated against the US dollar compared to the previous week. The baht's depreciation was less than that of other major currencies, resulting in the NEER index appreciating by 0.16% from the previous week.

Economic Indicators

Global Economic Indicators

Thank you for the information from the Macroeconomic Policy Bureau - Fiscal Policy Office, Ministry of Finance 02-273-9020 Ext. 3259